What the Reinsurance Industry Already Knew

/Daniel Kreeger | Posted October 18, 2024

I was on CGTN with Gerald Tan last week. Hurricane Milton made landfall at Siesta Key with 120 mph winds. Tampa avoided a worst-case storm surge because of a southward track, but the inland flooding was severe. St. Petersburg saw 18 inches of rain in 24 hours with more than three million customers losing power. The death toll is climbing and likely will for some time.

Our conversation covered a lot of ground, but there is one thread I want pull, because most coverage of the storm has not gotten to it yet.

The reinsurance industry has been pricing climate change into its models for over twenty years. The primary insurance industry, the part most visible to homeowners and small businesses, is only now catching up, and the catching up is producing the visible market disruption Floridians are living through. The gap between those two timelines is the story most people have missed.

Hurricanes Milton and Helene: 2 Weeks Apart, 2 Completely Different Stories

Florida's Gulf Coast was prepared for Milton. The communication from state and local officials was sharp. The bullseye sat over Tampa for several days. People moved to shelters. Infrastructure investments made over the past decade absorbed more than I expected. The damage is still significant, and people died, but the response performed at the level the situation required.

Compare that with Hurricane Helene, which just hit western North Carolina two weeks before. Helene dropped catastrophic rain on a region that does not think of itself as hurricane country. Asheville lost municipal water for weeks. Communities along the Toe and Swannanoa rivers were destroyed by flooding nobody had planned for at that scale. The death toll there is over 200 and still rising, and the recovery on this one will take decades and likely will not be anywhere near full.

Two storms, two weeks apart, very different outcomes. The difference is not just the storm. The difference is preparation, both immediate and long-term:

Florida has been investing in storm-water infrastructure, building codes, evacuation systems, and public communication for decades

Western North Carolina did not, because the historical risk was lower and the design assumptions reflected that

When the storm arrives somewhere it has not arrived before, those decades of preparation are not available

This is the operational reality of a destabilizing climate. Risk is shifting to places that did not previously face it, and those places are not ready.

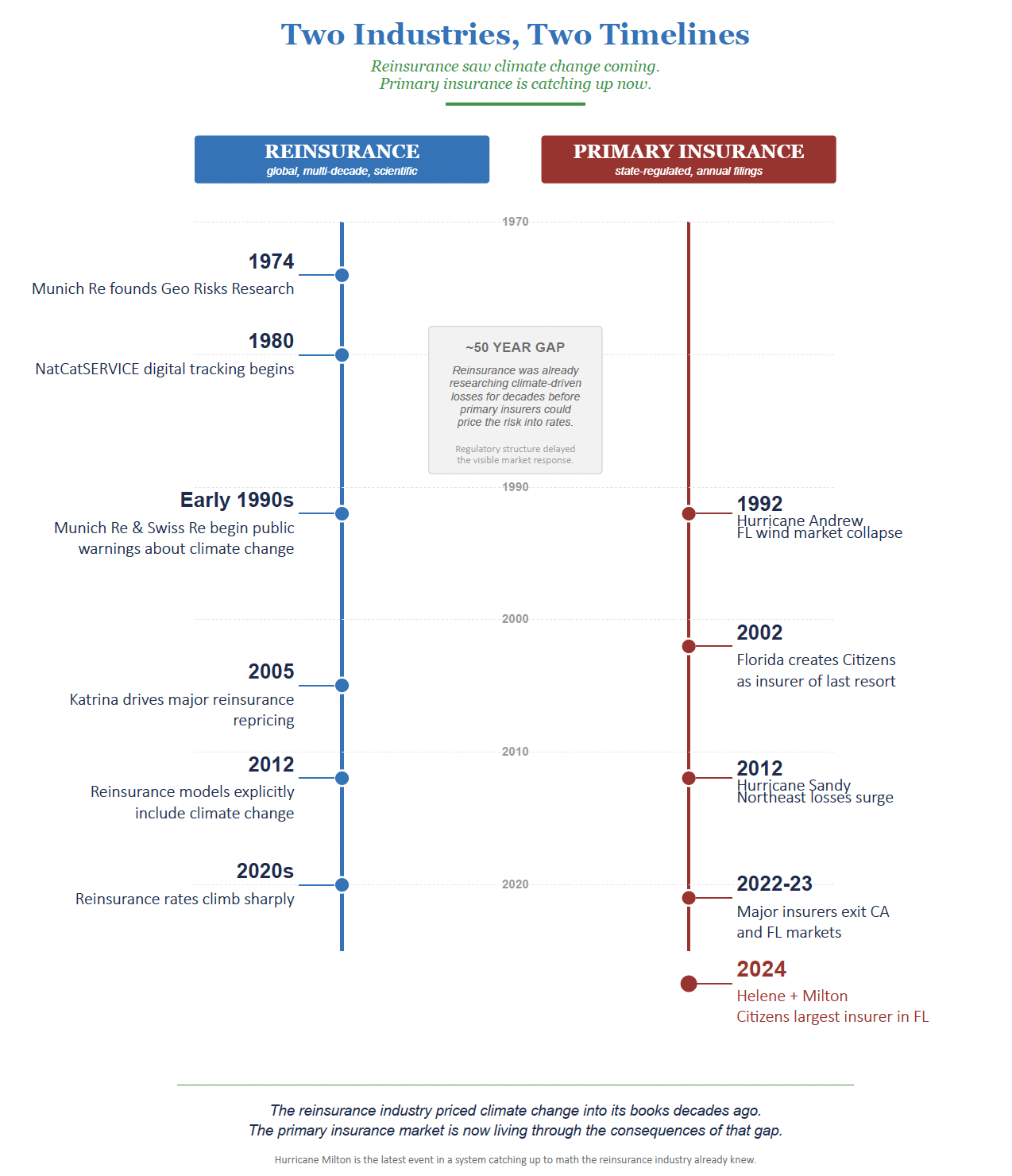

2 Industries, 2 Timelines

Most people think of "the insurance industry" as a single thing. It is not. The structural distinction matters.

Reinsurance is insurance for insurance companies. When a hurricane hits Florida, the primary insurer pays out claims to homeowners. The reinsurer covers a portion of those payouts according to contracts written in advance. Reinsurers operate at global scale, on multi-decade horizons, and across diversified geographies. Munich Re, Swiss Re, Hannover Re, and the Lloyd's of London market are the major players.

The reinsurance industry has been pricing climate change into its models since the 1980s. Munich Re's NatCatSERVICE database, which tracks natural catastrophe losses globally, has shown an unmistakable rising trend in climate-driven losses for decades. Reinsurers cannot hide from this trend because their books are explicitly designed to absorb tail risk. They have to model it accurately or they go out of business.

Primary insurance is the policy you write a check for every year. The company that pays you when your roof comes off. The companies that dominate this market, including Allstate, State Farm, and the various Florida-specific insurers, operate under a fundamentally different regulatory structure.

That structure is the part most people miss.

Why the Primary Insurers Lag Behind Reinsurers

Primary insurers in the United States are regulated at the state level. Each state's insurance commissioner reviews rate filings and approves what insurers can charge. The structure has several features that make it poorly suited to climate change:

Annual or short-cycle rate filings. Premiums are reviewed and approved year by year, or at intervals measured in a few years. The regulatory process emphasizes recent loss experience, not long-term forward-looking models.

Political pressure on rate increases. Insurance commissioners are elected officials in many states or appointed by elected officials. Approving large rate increases is politically costly, even when actuarially justified.

Restrictions on the use of forward-looking models. Several states explicitly limit the ability of primary insurers to use climate-projection models in setting rates. They are required to base rates on historical loss experience, even when the historical record is no longer predictive.

Customer expectations of stable premiums. The product is sold annually. Customers expect modest year-over-year changes. Sudden large rate increases trigger political backlash regardless of the underlying math.

These constraints made sense when climate risk was reasonably stationary. They do not work when the risk landscape is shifting faster than the rate structure can absorb.

The result is that primary insurers, watching their reinsurance costs rise sharply over the past two decades, have been caught between rising actuarial pressure and regulatory limits on what they can charge. Some have absorbed losses for years. Some have exited markets entirely. Some have narrowed coverage terms in ways that effectively shift risk back to homeowners. Some have failed and been absorbed into state-backed entities.

This is what the visible disruption in Florida's insurance market actually represents. Not insurers waking up to climate risk. Primary insurers running into the wall that reinsurers warned them about decades ago.

What Hurricane Andrew Taught Us in 1992

Florida saw a version of this dynamic in 1992 with Hurricane Andrew. Andrew was a Category 5 storm that flattened parts of South Florida. The destruction was catastrophic. The aftermath was structurally relevant.

In the months following Andrew, the private wind insurance market in Florida collapsed. Insurers pulled out of the state because they could not continue to write policies at any price that customers were willing to pay. Florida had to stand up Citizens Property Insurance Corporation, a state-backed entity that became the insurer of last resort for properties the private market would no longer cover.

Citizens has been a permanent feature of Florida's housing economy ever since. It has grown larger, shrunk again, and grown larger again, depending on which catastrophic events have most recently reshaped the private market's appetite. Right now, Citizens is again the largest insurer in the state.

Andrew was a single storm in a single place. The current dynamic is broader. The reinsurance signal is global and persistent, not a one-off event. The primary market disruption is showing up in many states, not just Florida, although Florida feels it most acutely. The structural fix from Andrew, a state backstop for what the private market would not write, is being stretched in ways it was not designed for.

What is Happening Now?

The lending industry is starting to follow the same path. Mortgage lenders are increasingly cautious about properties in high-risk areas. Some banks have begun pricing climate exposure into commercial lending decisions. Conversations about insurability and bankability that were rare five years ago are now standard in real estate transactions in coastal areas, wildfire-prone areas, and floodplains.

The skittishness in primary insurance and lending right now is happening for good reason. It reflects what the actuarial math has been saying for decades through reinsurance, finally working its way through to the visible consumer-facing parts of the financial system.

This is not ideological. It is mathematical. When the historical record stops being a reliable guide, both industries adjust. They do so quietly, in ways that do not make the front page, but the cumulative effect changes what gets built where.

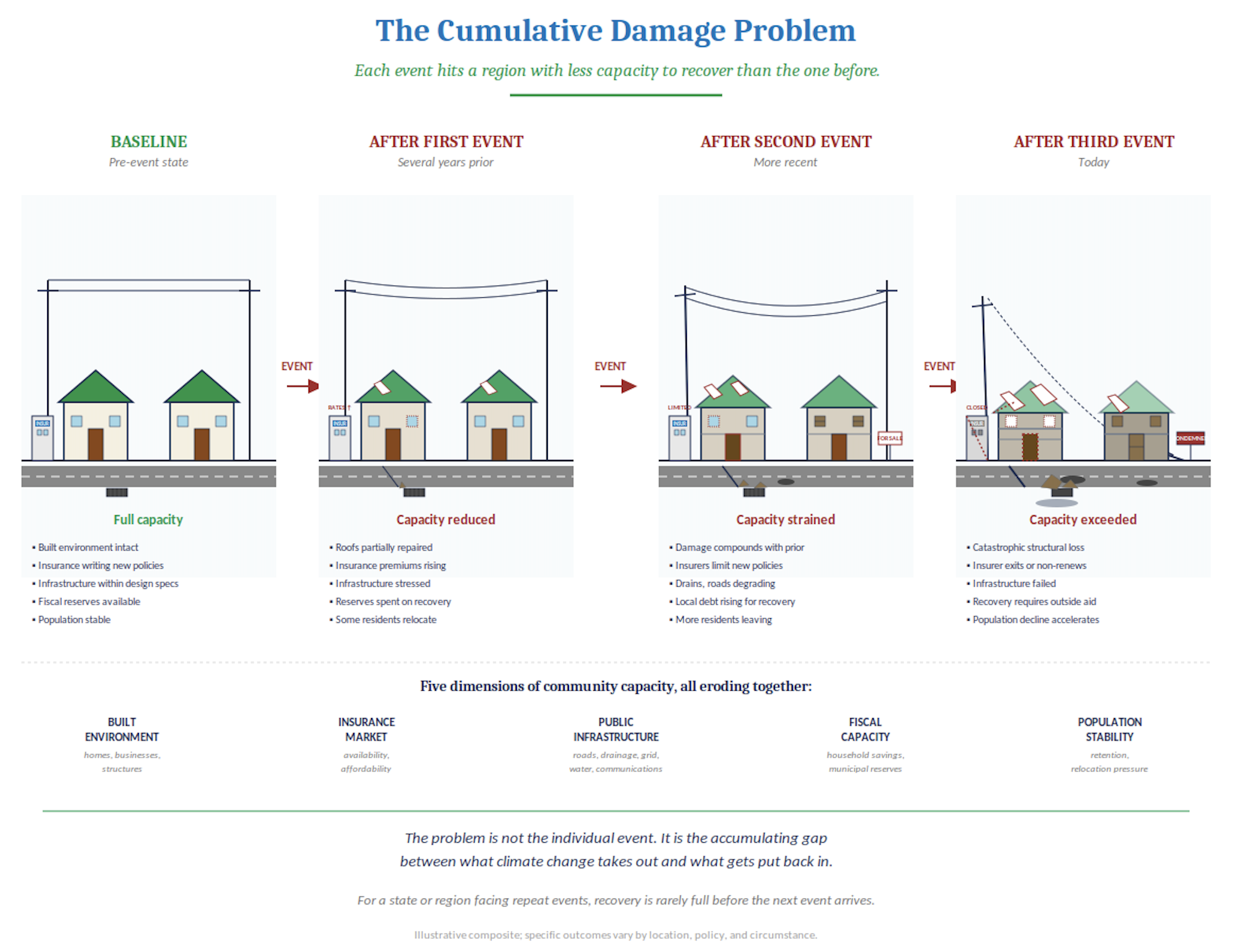

Cumulative Damage Compounds the Problem

The other operational reality with Milton is that this is not an isolated event. It is the latest in a sequence of events hitting overlapping geographies.

Some examples of how the cumulative effect actually shows up:

Debris from Helene's flood damage, never fully cleared, became projectile risk during Milton's high winds

Structures damaged by Hurricane Irma in 2017 that were never properly repaired sustained additional damage in this storm

Stormwater systems already operating beyond design capacity from previous events failed faster than expected this week

Insurance claims from prior storms that were settled at pennies on the dollar left properties underinvested in the resilience improvements that would have helped them this week

Communities that took on debt to recover from earlier events have less fiscal capacity to recover from this one

When my own family was hit by Hurricane Irma in 2017, my parents recovered about 30 cents on the dollar. That is what the math actually looks like for many people. You do not get back to where you were. You rebuild with less than you lost. The next storm hits a less-resilient property than the one before.

Multiply that by every property in every climate-exposed community, and the problem is not the individual storm. It is the accumulating gap between what climate change is taking out of these places and what is being put back in. The reinsurance industry has been modeling this gap for years. The primary market is now experiencing it.

What the Structural Fix Actually Requires

The path forward is structural. Three things have to happen at once.

Regulatory Modernization: State insurance regulation needs to allow primary insurers to use forward-looking climate models in setting rates, with appropriate consumer protection guardrails. The current structure produces volatility, not stability, because it forces premiums to lurch upward in response to single events rather than adjust gradually as the risk landscape shifts.

Smart Public Investment. Disaster recovery dollars should improve resilience, not just rebuild what was there before. Building codes and zoning ordinances should reflect future risk, not historical patterns. Public infrastructure for storm protection, water management, and grid resilience should be funded at scale that matches the actual risk environment.

Honest Private Capital. Lenders, insurers, and real estate investors all need to price climate risk honestly into their decisions. Some of this is already happening. Much of it is being delayed by short-term incentives or regulatory constraints that prevent honest pricing.

None of this is simple. None of it is fast. All of it is necessary if Florida, the Carolinas, and every other climate-exposed community are going to remain economically viable as the risk landscape continues to shift.

The reinsurance industry has been telling us this story for decades. The primary insurance industry is now learning to tell the same story to consumers, slowly, against the grain of a regulatory structure that was not designed for a non-stationary climate.

For communities making decisions today about where to build, where to invest, and how to plan, the most useful question is no longer whether climate change is real. The reinsurance market answered that question in the 1990s. The primary insurance market is answering it now. The useful question is whether the regulatory framework, the public infrastructure, and the private capital can be aligned fast enough to keep places livable as the risk landscape shifts.

That is the work. It is happening unevenly … and it needs to happen faster.

Watch the segment on YouTube →

— Dan